How patronising...shareholders don't know what's good for them and can't be relied upon to take the money and run. That's the message from the Alinta Board in rejecting Macquarie's bid. It's absolute rubbish. Seriously, if shareholders can't be bothered taking an interest in their investment it's their problem, go and buy managed funds.

I'm quite happy to take the cash and bolt for the exit, I've got zero interest in taking shares in various structured entities of which I have no idea how to value: are we seriously expected to take the word of B&B that these companies are worth what they say? Talk about conflicts of interest.

There's probably a few Fincorp investors on the Alinta register too. Bet they'd be keen to get their hands on the cash so they can throw it at some other dodgy scheme.

Saturday, March 31, 2007

Friday, March 30, 2007

Weird trading in Super Cheap Auto

Since I purchased shares in Super Cheap Auto mid way through last year the company has had a great run, doubling in price in a short space of time. But during this run I've noticed some strange trading patterns: small parcels of stock traded, often on an up-tick. There's been plenty of occasions where the shares have traded up strongly against the trend but on quite low volume.

I think the first time I really paid attention was around Christmas, but just put it down to the lack of liquidity over the holiday season. Well, it's on again. Here's some screen shots off E*Trade from trading yesterday (29/03/07). Firstly around 10.30 then around lunchtime.

You can see in the course of sales the very small parcels going through, quite a few of just one share. Not long after the second screen shot was taken a seller of 2 shares went in at 4.32.

You can see in the course of sales the very small parcels going through, quite a few of just one share. Not long after the second screen shot was taken a seller of 2 shares went in at 4.32.

Is it a coincidence that the two times I've noticed this have been around the end of a quarter?

I can't think of too many good reasons to be selling lots of 1 or 2 shares at a time, unless of course your goal is to get the price to a particular level, or keep it there. For example, if you were facing margin call, trade a small amount of volume at a higher (or lower) level. If that's the case, it's a form of market manipulation and ASX should be onto the case.

Although if it is an attempt at market manipulation it's a pretty amateurish one. Regardless, I am curious to know exactly what is going on here. If you've got any ideas let me know.

I still like the company on a fundamental basis though, as I don't think it's overpriced despite the good run. In reality it was heavily oversold and should never have fallen as far as it did.

I think the first time I really paid attention was around Christmas, but just put it down to the lack of liquidity over the holiday season. Well, it's on again. Here's some screen shots off E*Trade from trading yesterday (29/03/07). Firstly around 10.30 then around lunchtime.

You can see in the course of sales the very small parcels going through, quite a few of just one share. Not long after the second screen shot was taken a seller of 2 shares went in at 4.32.

You can see in the course of sales the very small parcels going through, quite a few of just one share. Not long after the second screen shot was taken a seller of 2 shares went in at 4.32.Is it a coincidence that the two times I've noticed this have been around the end of a quarter?

I can't think of too many good reasons to be selling lots of 1 or 2 shares at a time, unless of course your goal is to get the price to a particular level, or keep it there. For example, if you were facing margin call, trade a small amount of volume at a higher (or lower) level. If that's the case, it's a form of market manipulation and ASX should be onto the case.

Although if it is an attempt at market manipulation it's a pretty amateurish one. Regardless, I am curious to know exactly what is going on here. If you've got any ideas let me know.

I still like the company on a fundamental basis though, as I don't think it's overpriced despite the good run. In reality it was heavily oversold and should never have fallen as far as it did.

Thursday, March 22, 2007

Will the last Alinta bidder please turn out the lights?

So Bob Browning's jetting off to Mobile, Alabama to mess about with boats and Leighton's allegedly not playing. This should put Macquarie in a good position, assuming they can figure out a package that can be sold to co-investors (read patsies) as not being too greedy.

Alinta's shares have fallen off a bit back to $14 or so, so presumably all that talk of a 'killer' bid a couple of weeks ago - the stories suggested $9bn versus $7bn currently - was just that. Other media stories claimed the sources had mucked up Singapore dollars and Aussie dollars...nice work.

No doubt it will be something incredibly complex that involves pulling bits apart, reassembling them and relisting them with a couple of transaction fees in between. I'll be glad when the saga is over, can't wait for the bidding period to close and get out. Not that I, or any, Alinta shareholder should have too many financial complaints, the shares have done extremely well. Now, where to put the money? That is a problem for sure, but a nice one that I'm happy to have (kind of like a tax problem towards year end)

Alinta's shares have fallen off a bit back to $14 or so, so presumably all that talk of a 'killer' bid a couple of weeks ago - the stories suggested $9bn versus $7bn currently - was just that. Other media stories claimed the sources had mucked up Singapore dollars and Aussie dollars...nice work.

No doubt it will be something incredibly complex that involves pulling bits apart, reassembling them and relisting them with a couple of transaction fees in between. I'll be glad when the saga is over, can't wait for the bidding period to close and get out. Not that I, or any, Alinta shareholder should have too many financial complaints, the shares have done extremely well. Now, where to put the money? That is a problem for sure, but a nice one that I'm happy to have (kind of like a tax problem towards year end)

Rates up once? anyone for twice?

Well we're nearly back to 6000 courtesy of a 1.5% gain on Wall St which in turn was in response to Fed comments that seem to indicate the tightening bias might be over. In turn US rate cuts could be on the agenda...I don't think they'll get back to 1% again but one or two moves might be in order.

Meanwhile Australia could be going in the reverse direction. The normally staid interest rate markets went into a flat spin last Friday morning after comments by RBA Assistant Governor Edey were interpeted to mean our cash rate may yet move up again, getting it to 6.50%. Talk about turmoil...we've gone from 'rates are going nowhere' to ' rates are going up' in a flash. This has been good for the Aussie dollar, which has gone through US80 cents and even spiked a bit after the Fed's comments overnight. Hmmm, that's not doing my overseas plans much good!

Theoretically, rising rates should put a crimp on valuations. But in practice, the long end of the yield curve hasn't risen as much as the short with the gap between long and short rates widening quite a bit. So that probably means it's not going to do too much damage from that perspective. Even though corporate gearing is increasing, either as a way to to fend off private equity raiders or because of them, one more RBA move won't cause interest expenses to dampen profits too much.

Of more concern would be the possible effect on household demand and the flow on effect to sales. Given the strength of household demand - just look at the last set of national accounts, and look around you at the new plasma screen the Jones' have just bought - maybe one more hike won't be enough, maybe the momentum we've got will require the RBA to act twice, or more! Now that would be interesting: two rate rises, in an election year, with an election budget coming up in May (and I don't care what Costello says, there's no way that budget is going to be disciplined, not with Rudd creeping up in the polls!)

Meanwhile Australia could be going in the reverse direction. The normally staid interest rate markets went into a flat spin last Friday morning after comments by RBA Assistant Governor Edey were interpeted to mean our cash rate may yet move up again, getting it to 6.50%. Talk about turmoil...we've gone from 'rates are going nowhere' to ' rates are going up' in a flash. This has been good for the Aussie dollar, which has gone through US80 cents and even spiked a bit after the Fed's comments overnight. Hmmm, that's not doing my overseas plans much good!

Theoretically, rising rates should put a crimp on valuations. But in practice, the long end of the yield curve hasn't risen as much as the short with the gap between long and short rates widening quite a bit. So that probably means it's not going to do too much damage from that perspective. Even though corporate gearing is increasing, either as a way to to fend off private equity raiders or because of them, one more RBA move won't cause interest expenses to dampen profits too much.

Of more concern would be the possible effect on household demand and the flow on effect to sales. Given the strength of household demand - just look at the last set of national accounts, and look around you at the new plasma screen the Jones' have just bought - maybe one more hike won't be enough, maybe the momentum we've got will require the RBA to act twice, or more! Now that would be interesting: two rate rises, in an election year, with an election budget coming up in May (and I don't care what Costello says, there's no way that budget is going to be disciplined, not with Rudd creeping up in the polls!)

Wednesday, March 14, 2007

Shared equity open for business

Also yesterday we saw the release of another shared-equity style home loan product. This one is offered by the Macquarie-backed Rismark via Adelaide Bank. From an investment perspective I like these ideas because I think they have the potential to open up a new frontier (how exciting!). St George and Australand also announced a variation that splits the mortgage between two titles.

I have never seriously considered investing in property mostly because I don’t want to deal with tenants and the transaction costs really scare me off even with tax benefits and the excellent returns that have been generated. Not to mention the enormous punt you are taking on your ability to pick a half-decent property.

Obviously this mindset has cost me a mountain of money in the past five or six years (add that to the behavioural finance list of problems). So I think the prospect of property market indices and a related derivatives market is enticing. I’m assuming you could leverage up at the same ratios you would for standard property. There’s no reason why you shouldn’t be able to, particularly if you can spread your risk across different cities. I guess you miss out on rental income as there doesn’t seem to be an imputed rent attached but you should be able to still gain tax benefits.

Back to the share market, and one company front of the queue to benefit is RP Data. They are involved with Rismark and the property derivatives market. RPX were listed by way of a sell down by

More small cap action

Yesterday I took advantage (I hope) of weak pricing for one of my favourite small caps and bought some more. So far so good: no sign of any buyer’s remorse although at the time of writing the market hasn’t opened and I see the SPIs are down 90pts after more excitement overseas. I may be singing a different tune this afternoon!

The fundamentals of this particular company are excellent and my weighted average entry price is well below my valuation so even if it sinks further I’m quite happy to buy more and wait it out. The half year result last month gave all the indications they are on the right track, financially and operationally. Wish me luck.

Saturday, March 10, 2007

Time for an update

Thought it was time for an update to some of the issues that have been kicked around over the past couple of months.

Let’s start with Qantas. As expected, the Federal Government has given the seal of approval to the takeover of Qantas by the private equity consortium. Despite this the prospect of two institutional shareholders refusing to accept means that the bid still isn’t seen as a certainty, leaving the share price at a 21c discount to the dividend-adjusted bid price of $2.45. So buying now could deliver a gain of approximately 4% assuming the takeover goes through. Qantas lost 7c on Friday and if the drop became a bit overdone it could be worth a go.

Cardno was flagged as a stock for the watchlist with the caveat that it was priced for growth. In my opinion the company needed to deliver EBIT growth of 17% p.a. over the next decade to justify a then-share price of $6.10. Since then it has released some half yearly results which seemed to indicate that EBIT grew by only 6.3% for the half. NPAT on the other hand was up 16.3% with the bottom line benefiting from lower effective tax rate and lower financing costs. It looked like the company’s financial position improved over the half with debt servicing stronger and working capital improvements. I am a bit puzzled with one aspect of its cashflow so that will need a bit more investigation. However the bottom line is the share price had a bit of a run up leading to the profit release, hitting $6.50 albeit on light volume. Since then it’s fallen perhaps 10% and now trades at $5.87. In my opinion it’s still overpriced but I’m happy to keep an eye on it.

Towards the end of January I looked at BHP, then trading at $25.33, from which point it’s since rallied perhaps 10-15% and still seems to be a broker favourite.

And lastly, I’ve talked about my reasons for selling one of my small cap stocks. It was a tough decision but one I’m glad I made. The little fellah has lost 15% since I bailed.

Actually on the topic of small caps during the correction at the end of February I noted in a post that liquidity in my small caps just evaporated – in a couple of cases it hasn’t returned. Spreads are still enormous and there’s no volume to speak of. Maybe it’s stock specific? I’ll have a look around, but if anyone else has noticed this with their favourites please let me know (no, you don’t have to tell me what they are). There might be some good companies on the cheap in that segment so I’m going to put some energy into that over the next few weeks.

Let’s start with Qantas. As expected, the Federal Government has given the seal of approval to the takeover of Qantas by the private equity consortium. Despite this the prospect of two institutional shareholders refusing to accept means that the bid still isn’t seen as a certainty, leaving the share price at a 21c discount to the dividend-adjusted bid price of $2.45. So buying now could deliver a gain of approximately 4% assuming the takeover goes through. Qantas lost 7c on Friday and if the drop became a bit overdone it could be worth a go.

Cardno was flagged as a stock for the watchlist with the caveat that it was priced for growth. In my opinion the company needed to deliver EBIT growth of 17% p.a. over the next decade to justify a then-share price of $6.10. Since then it has released some half yearly results which seemed to indicate that EBIT grew by only 6.3% for the half. NPAT on the other hand was up 16.3% with the bottom line benefiting from lower effective tax rate and lower financing costs. It looked like the company’s financial position improved over the half with debt servicing stronger and working capital improvements. I am a bit puzzled with one aspect of its cashflow so that will need a bit more investigation. However the bottom line is the share price had a bit of a run up leading to the profit release, hitting $6.50 albeit on light volume. Since then it’s fallen perhaps 10% and now trades at $5.87. In my opinion it’s still overpriced but I’m happy to keep an eye on it.

Towards the end of January I looked at BHP, then trading at $25.33, from which point it’s since rallied perhaps 10-15% and still seems to be a broker favourite.

And lastly, I’ve talked about my reasons for selling one of my small cap stocks. It was a tough decision but one I’m glad I made. The little fellah has lost 15% since I bailed.

Actually on the topic of small caps during the correction at the end of February I noted in a post that liquidity in my small caps just evaporated – in a couple of cases it hasn’t returned. Spreads are still enormous and there’s no volume to speak of. Maybe it’s stock specific? I’ll have a look around, but if anyone else has noticed this with their favourites please let me know (no, you don’t have to tell me what they are). There might be some good companies on the cheap in that segment so I’m going to put some energy into that over the next few weeks.

Friday, March 2, 2007

Just a pitstop on the road to prosperity?

Rather than simply repeat what’s happened this week, I’d prefer to try and figure out if it actually means anything or whether it’s just another pitstop on the road to prosperity.

Personally I don’t buy the broker-spin peddled in some news outlets about it being a “healthy correction”. I think it’s a warning sign that things in the ‘hood aren’t going to quieten down in a hurry. After all, something of an overreaction don’t you think? An over-inflated market has a rumour-driven sell off yet investors fromNew York to Sydney I believe the problems are deeper than the toasting of some Chinese retail investors and the ubiquitous hedge funds. Several aspects of it are troubling and I’m still organising my thinking but here’s where I’m at:

Personally I don’t buy the broker-spin peddled in some news outlets about it being a “healthy correction”. I think it’s a warning sign that things in the ‘hood aren’t going to quieten down in a hurry. After all, something of an overreaction don’t you think? An over-inflated market has a rumour-driven sell off yet investors from

- The yen carry trade is a big source of liquidity for global markets. Yen-denominated borrowings are invested in securities of higher yielding currencies (AUD, USD, NZD for example)

- The

- Asset backed securities have been a destination of choice for carry-trade proceeds so when those same securities start losing their value quickly thanks to defaults, how will the yen borrowings be repaid? By selling other securities, that’s how

- The yen has had a bit of a rally lately, reflecting many of these factors. If it gains momentum it will simply exacerbate some of the problems

- And because so many investors, funds and banks have put on this trade, if there are forced sales then it will get nasty

Firstly, who looked at their small cap stocks? Spreads ballooned from maybe 3-5 cents out to 30 cents+ as liquidity just vanished. A few of mine were down dramatically on miniscule volume thanks to what must have been a panicky retail investor selling everything that moves. I kind of hope we get some more of this because there will be some great little companies available for good prices, provided you can be patient.

Secondly, the enormous gaping flaw of using online brokers was again exposed: when things are bad, you haven’t got a hope of getting reliable service from their website. E*trade was having problems and I gather Commsec was too. More upgrades I guess. Anyone know exactly when E*trade’s new new website will finally be launched?

Sunday, February 25, 2007

Five ways to invest overseas

Regular readers will know that right now I’m a big fan of diversifying away from Australia into overseas markets. In my quest to promote this idea I decided to find five ways you can get offshore without learning French or catching the dreaded Delhi belly.

Personally I’ve preferred options 1 and 5 for true investing leaving 2 & 3 for dabbling and entertainment.

- Managed funds – No kidding you say, but what sort? I think a good active manager should be able to pick which international markets are on the up in the medium term (I like Europe and Asia over the US). Long term most of the active guys will probably come back to the pack but now I think the timing is right for actives because international index funds are often based on MSCI ex Australia so will have too much in the US for my liking. I always check the fund manager’s view on hedging. Most funds provide the manager with a discretionary range to hedge (e.g. 30-70%) while others have a firm policy.

- CFDs – plenty of alternatives are available here. If you're not familiar with CFDs get a flavour from one of my previous posts. Depending on the provider you can go from FTSE to DJIA through to indices in India and Shanghai. Most will offer a crack at straight index plays or get into the noxious world of binaries (a.k.a. bet options). And speaking of bet options…

- Betfair – I’m not joking, provided you’re not an AFL footy player you can bet on financial markets, including overseas interest rates and stock indices. Granted, it’s not exactly long term investing when you’re playing the hourlies, but you can do it. The Financials forum often has some spicy conversations with punters railing against rogue bots amongst many other things. This is strictly for entertainment.

- Index warrants – listed on the ASX with market makers happily making a price on either side for you. Call and/or put warrants are usually available over the Nikkei, S&P500 and Nasdaq.

- Overseas companies listed on the ASX – News Ltd is a great example of a stock where the drivers are primarily international. James Hardie and Rinker are two more. Also look at some of the property trusts, Babcock & Brown Japan is one example, Macquarie’s Prologis and DDR are two others that come immediately to mind (and please remember these aren’t recommendations, they’re examples)

Personally I’ve preferred options 1 and 5 for true investing leaving 2 & 3 for dabbling and entertainment.

Monday, February 19, 2007

Diary of a CFD trader: 5 days in the life

Or: how I went short in a rampant bull market and survived (just!)

Back in April/May 2006 I felt the rally was becoming overdone. I originally began shorting the market using index warrants with some success but then constant Weekend AFR Smart Money articles convinced me to open a CFD account and try using contracts over the ASX 200 instead. It was to be my first experience with the now ubiquitous CFD and I was spurred on by frustration with the market maker’s warrant pricing.

I felt that the index would return to around 5000-5100 so my strategy was to short the index after rallies. As I was betting against the trend one of my risk management exercises was a rule that I had to be square at the end of each day. I wasn’t prepared to risk being short overnight and have the market move 60-80 points against me.

So, without further ado, here are my notes from five different days of trading CFDs:

Day 1: Friday

The market fell sharply the previous day (1.6%) so I figured I could sell into a recovery rally. The open was strong, wiping out almost all of the prior days losses. I figured it wouldn’t hold and sure enough, shortly after opening fell back. Opened my position at 42.5 and fifty minutes later I’m closed out at 26.0. Great way to start, I'm stoked.

Later in the morning we get another small rally, so I try again this time opening up at 35.0 but get stopped out ten points higher. Finish the day mildly square, up six points, but what fun!

Day 2: Tuesday

Dead keen to get into the action again, the market opens and quickly unwinds the 1.2% rally of the previous day. Using my highly tuned instincts (with a full one day’s CFD trading under my belt) I decide that 31.0 looks like a good spot to open another short position. The market trades in a tight range and I’m out of the money for most of the day. As we get near to close it finally drops off and I buy my contracts back at 16.0 finishing up 15 points. Two from three!

Day 3: Friday

Tight trading ranges since Tuesday haven’t offered many opportunities but big falls offshore overnight suggest today could be a good one. I use a fairly tame opening to get set at 19.0 and then add to my position at 18.0 – three days into this adventure and the confidence levels are sky high – before watching it move sharply against me: my stops were triggered on the first position but I let the second run – big mistake – and wind up down 11.5 points on the first and 21.5 points on the second. Ouch, there are a few naughty words sprayed around. Later in the day as the late morning rally runs out of steam I try again and sell more contracts at 27.0 and then towards close sell more at 7.5. The market closes, stops are in place and I’m watching the overnight session to try and get out square. It’s getting late but I really really want to make that money back. It’s not until 11pm I finally give in and close both at 3.5. I’m down just six points for the day. Phew, big relief after a nasty start to the morning and I feel like I’ve done well as we go into the weekend.

Day 4: Monday

It’s all one way traffic today. Big falls on Friday night as major markets lose more than 1.5%. I get in as quick as I can and sell at 37.5 but too late, the market has already bottomed and the best I can do is make just 6.5 points for the day. It’s a golden opportunity squandered because the market’s finished nearly 100 points under the level at which I closed out my positions on Friday: damn it, should have stayed up later last week (more coffee!) or just left them alone entirely! More creative swearing ensued, big profit opportunity missed. In fact, I missed out on profiting from the entire reason I’ve been trading the damn things!

Day 5: Wednesday

Throwing strategy and plans totally out the window I go long expecting a “dead cat bounce” and I’m set at 22.0. The market hovers, falls scarily close to my stop before recovering and looking good. I buy more at 22.0 as it goes through and ride it for the rest of the morning. Just before lunch I call stumps and sell at 42.0. The market has moved as high as 50.0 before falling back. It’s looking a lot weaker now with selling increasing so I take my profits and run. A good day out, made 20 points on each position and I debate reversing and going short but decide it should hold its ground. Alas, wrong again, the market promptly plummets in the afternoon and finishes at 17.5.

Epilogue:

Not long after the fifth day the market closed at 5100 so it was back down to where I expected it to be. I packed up my toys and went home, putting the CFD capital and gains into something less exciting. However as history shows the market then went on to fall even further, getting down to 4838 by mid-June so I should have stayed in there but of course the index has put on over 1000 points since then so I guess I can’t really complain one way or the other.

Ultimately I made twice the money from my warrant trading than CFDs for about half the effort but on recollection (gotta love the rose coloured specs) I think I enjoyed the CFDs a whole lot more.

I learned a lot from this little exercise but it’s particularly interesting how my trading rules (e.g. squaring up at the end of each day) worked against me in some ways and actually stopped me from getting the really big profits that my strategy would have delivered if I’d stayed with warrants. I guess because it was a new instrument to me that I was a bit more cautious than usual, plus the fact that the leverage on these things is huge. And on the flip side the rule probably protected me from some of the big upward moves overnight. Next time I think I should be prepared to take on more risk.

Friday, February 16, 2007

Strategy & outlook

Amongst the lively prose in this week’s RBA’s quarterly Statement on Monetary Policy were some useful figures on equity market valuation and the outlook for share market drivers.

PE ratios and yields seem to be around about long term average levels. Our PE ratios are consistent with the rest of the world but yields measurably higher; likely a reflection of our dividend imputation system.

According to the RBA, analysts are forecasting EPS increases of 14% for the ASX200 in the 2006/07 year but only 7% in 2007/08.

Meanwhile leveraged buyout (LBO) activity is seen as a key driver of recent performance with the central bankers citing the relatively low cost of debt compared to ROE. Even though we saw three rate hikes last year, long term bond yields remain low. The Bank believes excess demand is the primary reason long term rates remaining so low (10y yields 40-45bp under cash). Reflecting some level of concern about the private equity jockeys the bank points out that excessive leverage increases the risks to macroeconomic stability.

The outlook for commodities, specifically metals and energy is of critical importance. In the past three months we have seen 25% falls in copper and oil, partially reflecting a deflating speculative bubble but also some changes to the supply/demand dynamics. Growth in copper production now exceeds growth in demand. With new supplies for coal and other commodities coming online in the next 12-18 months the Bank believes we are unlikely to see much more price growth from any of these minerals.

Lastly, the outlook for inflation has the headline rate expected to fall below 2% by mid year. If this occurs then my pick is that rates could begin falling sometime late in 2007 or early 2008. With overseas rates increasing (Europe, for example) and a likely drop off in commodity prices over 2007/08 the AUD can be expected to fall over 2007 making this an excellent time – as I’ve mentioned before – to start diversifying out of the Australian equity market and getting into overseas markets, unhedged, or choose stocks with significant offshore exposure and revenue streams.

While the profit growth prospects for the Australian market generally are good for 2006/07 results, 2007/08 is modest (7%). From about now on, markets will be looking to 2007/08 numbers for valuations. If the outlook statements from the current reporting season suggest earnings growth greater than expectations then the market should hold up for another few months but beyond that I think we have to seriously question where additional growth and momentum in earnings – for the market generally – is going to come from.

The ‘weight of money’ thesis argues that the large volume of funds pouring into super and other investment vehicles will keep the market buoyant. That’s true but only to a point. As soon as returns disappear or the risk increases the money will look for a better home. Right now the tolerance for risk is high, evidenced by very low credit spreads and low volatility in the markets so the money is flowing in but that could reverse quickly – don’t get caught looking the other way when it does!

Currently I’ve got 20% international equities, 65% Australian equities and 15% cash. I’d be happy seeing overseas rise to 25% or even 30%. Disagree? Leave a comment!

Wednesday, February 14, 2007

Building a better investor

It’s tempting to look back on the good performers in a portfolio and wonder why you didn’t buy more. I rationalise that thought with the knowledge that if I had bought more of XYZ Ltd I wouldn’t have had enough resources to buy other companies which may have delivered similar or better results.

But it raises an interesting issue. When should you add to an existing position? I recall a conversation I had some years ago with a professional technical trader – let’s call him Ed – who was day-trading local and international markets long before the term was invented. Ed was always on the lookout in his charts for signs of strength. He was, and still is a momentum trader but he got very excited on finding one of his winning positions was showing what he termed a second buy signal. When this happened Ed would usually more than double his existing stake and promptly head out for a long lunch secure in the knowledge he was onto a major winner.

The discipline of technical trading systems is to my mind a major strength when compared to standard fundamental analysis approach. Often there is a psychological barrier of having bought at a much cheaper level and then not wanting to buy more until it returns there, even though it makes no sense.

Similarly, how often have you had your confidence shaken when, after buying a stock, it promptly loses 10-15%? If nothing has changed why wouldn’t you buy more? After all, your expected return has just gone up. Barton Biggs dealt with this question in his excellent story of life in the markets Hedgehogging. One of the trading rules of his hedge fund was that if a position lost 10% they either had to sell half or buy more. Whatever the outcome, the position is reviewed so the rule works by forcing action whereas the default outcome for most investors is to cross appendages and hope for the best.

I found another example of strange investor behaviour during the Telstra 3 float last year. I asked people who planned to subscribe whether they would have considered buying Telstra on market if it fell to $3.30-$3.40 (the approximate present value price of T3) and all replied in the negative. Most saw T3 as a totally separate trade even though it’s the same company, they didn’t see it as adding to an existing position. The souped up yield probably helped. And yes, I bought T3 too.

Perhaps the issue is best dealt with as a simple rate of return problem. Upon calculating the value of a stock I can therefore estimate what my total return should be, assuming the market price eventually moves toward the target price. Therefore provided the returns available from the stock in question exceed the return trade off from the other companies under review I should buy more. Otherwise I may as well buy something else to diversify my risk.

Quirks in the human decision making process such as I have described contribute to the wide but interesting field of study known as behavioural finance. There’s plenty of research available that’s worth exploring further and at least one well known Australian fund manager uses behavioural finance themes in their advertising campaigns. I think the topic also has some relevance in the context of the “Mr Market” story made famous by Benjamin Graham.

Understanding your investment inhibitions is, I believe, a good step towards becoming a better investor. The lesson I’ve drawn from Ed (and Barton Biggs) is the benefit of introducing discipline and removing emotion and preconceived ideas from decision making. At the very least be aware of your own drawbacks and develop systems to counteract your natural tendencies.

But it raises an interesting issue. When should you add to an existing position? I recall a conversation I had some years ago with a professional technical trader – let’s call him Ed – who was day-trading local and international markets long before the term was invented. Ed was always on the lookout in his charts for signs of strength. He was, and still is a momentum trader but he got very excited on finding one of his winning positions was showing what he termed a second buy signal. When this happened Ed would usually more than double his existing stake and promptly head out for a long lunch secure in the knowledge he was onto a major winner.

The discipline of technical trading systems is to my mind a major strength when compared to standard fundamental analysis approach. Often there is a psychological barrier of having bought at a much cheaper level and then not wanting to buy more until it returns there, even though it makes no sense.

Similarly, how often have you had your confidence shaken when, after buying a stock, it promptly loses 10-15%? If nothing has changed why wouldn’t you buy more? After all, your expected return has just gone up. Barton Biggs dealt with this question in his excellent story of life in the markets Hedgehogging. One of the trading rules of his hedge fund was that if a position lost 10% they either had to sell half or buy more. Whatever the outcome, the position is reviewed so the rule works by forcing action whereas the default outcome for most investors is to cross appendages and hope for the best.

I found another example of strange investor behaviour during the Telstra 3 float last year. I asked people who planned to subscribe whether they would have considered buying Telstra on market if it fell to $3.30-$3.40 (the approximate present value price of T3) and all replied in the negative. Most saw T3 as a totally separate trade even though it’s the same company, they didn’t see it as adding to an existing position. The souped up yield probably helped. And yes, I bought T3 too.

Perhaps the issue is best dealt with as a simple rate of return problem. Upon calculating the value of a stock I can therefore estimate what my total return should be, assuming the market price eventually moves toward the target price. Therefore provided the returns available from the stock in question exceed the return trade off from the other companies under review I should buy more. Otherwise I may as well buy something else to diversify my risk.

Quirks in the human decision making process such as I have described contribute to the wide but interesting field of study known as behavioural finance. There’s plenty of research available that’s worth exploring further and at least one well known Australian fund manager uses behavioural finance themes in their advertising campaigns. I think the topic also has some relevance in the context of the “Mr Market” story made famous by Benjamin Graham.

Understanding your investment inhibitions is, I believe, a good step towards becoming a better investor. The lesson I’ve drawn from Ed (and Barton Biggs) is the benefit of introducing discipline and removing emotion and preconceived ideas from decision making. At the very least be aware of your own drawbacks and develop systems to counteract your natural tendencies.

Monday, February 12, 2007

Qantas rolls over

Updating my earlier post on the Qantas bid, aside from anything else I just hope management don’t trip over themselves or any stray Alinta executives in their rush to take the company private!

The independent expert’s report values the airline anywhere from $5.18 to $5.98 thereby conveniently placing the midpoint 2 cents under the $5.60 bid price. Good work, Grant Samuel & Board. A bit of a wider valuation range than we might have expected at more than 7% either side of the midpoint, but fairly tidy.

Looking back I admit at being slightly amazed just how fast the Directors rolled over and allowed the consortium in with just a 2% (10 cent) increase of their $5.50 original bid (compare it to Coles). Then I read the AFR on Friday February 9 with all the gory details of the success fees coming after another profit upgrade and I really wonder: was anyone looking out for the shareholders in this transaction?

I must point out that I’m not against the deal per se but I think some of the lousy behaviour present in the markets nowadays is clearly evident in this case.

The only real hurdle to success now is the FIRB – due to rule by March 7 – and Peter Costello who can make a ‘national interest’ ruling. For interest, the FIRB have raised no objections to most takeovers in the past few years including Xstrata/MIM, Singapore Telecommunications/Optus, and the BHP/Billiton merger. Famously, the Shell/Woodside deal was knocked back by the Treasurer but I doubt it will happen in this case.

The independent expert’s report values the airline anywhere from $5.18 to $5.98 thereby conveniently placing the midpoint 2 cents under the $5.60 bid price. Good work, Grant Samuel & Board. A bit of a wider valuation range than we might have expected at more than 7% either side of the midpoint, but fairly tidy.

Looking back I admit at being slightly amazed just how fast the Directors rolled over and allowed the consortium in with just a 2% (10 cent) increase of their $5.50 original bid (compare it to Coles). Then I read the AFR on Friday February 9 with all the gory details of the success fees coming after another profit upgrade and I really wonder: was anyone looking out for the shareholders in this transaction?

I must point out that I’m not against the deal per se but I think some of the lousy behaviour present in the markets nowadays is clearly evident in this case.

The only real hurdle to success now is the FIRB – due to rule by March 7 – and Peter Costello who can make a ‘national interest’ ruling. For interest, the FIRB have raised no objections to most takeovers in the past few years including Xstrata/MIM, Singapore Telecommunications/Optus, and the BHP/Billiton merger. Famously, the Shell/Woodside deal was knocked back by the Treasurer but I doubt it will happen in this case.

One for the watchlist

I like the concept of investing along a theme. It’s not new, but the strategy involves picking a trend then trying to spot companies exposed to the idea. You can often find a number of businesses in a particular market segment so either pick the best or spread your risk and buy everything. Two themes I’ve used successfully include agriculture – a contrarian play as the sector was then, as now, in the grips of drought – and smaller retailers who were expanding their store networks.

My latest theme is water, something very topical at the moment: we even have a new

Federal Minister for Environment and Water Resources while there have been some research papers on the economics of water released in the last few months. For one example, see ANZ’s Water use and regulation.

Regardless of what happens to control of the Murray River it’s very likely that there will be more construction of water treatment plants for recycling and desalination. While household consumption of recycled water will be some time off, industrial users won’t be too far away if the costs stack up. Companies with proven expertise in these projects should be front runners to pick up some business, while there will also be opportunities for companies who supply and install pipes. Some of the obvious candidates who should benefit from new projects are listed below:

But these are all bigger companies and it would take a few large projects to make a real difference to long term value. I like the idea of tackling some of the smaller players who might be more leveraged to new projects, and one that came up was Cardno (CDD), a firm with a background in engineering consulting but these days also involved in international assistance programs. If you know a little about Coffey (COF) you’ll find Cardno’s story familiar.

Cardno came to my attention through its involvement in the Gold Coast desalination plant but they are also working on the privatisation of the Abu Dhabi Sewerage Service in the UAE amongst other water-related things. If we start thinking about what Australia will need to do with water, these are exactly the type of skills required.

Their market cap is about $300M so maybe two-thirds that of Coffey and generating revenue close to $200M. Unfortunately it’s priced for growth with a capital G. I calculate Cardno needs average growth in earnings of around 17% over the next 10 years to justify current pricing of $6.12 or so. With the number of acquisitions undertaken in the last few years it’s not necessarily impossible but it’s also a big ask. That’s a shame, late last year it was under $5.00 and would have been a good pick up.

I like the mix of businesses which looks nicely diversified across different sectors making direct competition tricky. I like the skillset they own with the experiences gained overseas easily transferable to wherever growth is occurring and I think the specialised consulting services industry is quite fragmented providing opportunities to mop up and eventually expand margins.

One of the problems this type business can face is that while growing quickly they often chew up enormous amounts of working capital, a function of the accounts payable cycle (think wages, contractors etc) being a lot shorter than the collection cycle which on large projects can be measured in months rather than days. As a consequence, they are more likely to tap the markets for an equity top up and profit growth can’t always match revenue growth because of growing interest expenses. In Cardno’s case gearing is reasonable at 55% (June 06 figure, net debt) but interest cover is good at more than 5x so they could take on a bit more debt. Once the growth phase slows and investment in working capital stabilises the firm should be able to generate more surplus cash and paydown debt fairly quickly.

I think it’s expensive at over $6.00 having run up strongly in the past couple of months but I’m interested enough to add it to the watchlist and keep working on my research. If the growth embedded in the price comes back to low-mid double digits or new information comes to light I’ll be interested.

My latest theme is water, something very topical at the moment: we even have a new

Federal Minister for Environment and Water Resources while there have been some research papers on the economics of water released in the last few months. For one example, see ANZ’s Water use and regulation.

Regardless of what happens to control of the Murray River it’s very likely that there will be more construction of water treatment plants for recycling and desalination. While household consumption of recycled water will be some time off, industrial users won’t be too far away if the costs stack up. Companies with proven expertise in these projects should be front runners to pick up some business, while there will also be opportunities for companies who supply and install pipes. Some of the obvious candidates who should benefit from new projects are listed below:

- Leighton

- Multiplex

- United Group

- Transfield Services

- GUD

But these are all bigger companies and it would take a few large projects to make a real difference to long term value. I like the idea of tackling some of the smaller players who might be more leveraged to new projects, and one that came up was Cardno (CDD), a firm with a background in engineering consulting but these days also involved in international assistance programs. If you know a little about Coffey (COF) you’ll find Cardno’s story familiar.

Cardno came to my attention through its involvement in the Gold Coast desalination plant but they are also working on the privatisation of the Abu Dhabi Sewerage Service in the UAE amongst other water-related things. If we start thinking about what Australia will need to do with water, these are exactly the type of skills required.

Their market cap is about $300M so maybe two-thirds that of Coffey and generating revenue close to $200M. Unfortunately it’s priced for growth with a capital G. I calculate Cardno needs average growth in earnings of around 17% over the next 10 years to justify current pricing of $6.12 or so. With the number of acquisitions undertaken in the last few years it’s not necessarily impossible but it’s also a big ask. That’s a shame, late last year it was under $5.00 and would have been a good pick up.

I like the mix of businesses which looks nicely diversified across different sectors making direct competition tricky. I like the skillset they own with the experiences gained overseas easily transferable to wherever growth is occurring and I think the specialised consulting services industry is quite fragmented providing opportunities to mop up and eventually expand margins.

One of the problems this type business can face is that while growing quickly they often chew up enormous amounts of working capital, a function of the accounts payable cycle (think wages, contractors etc) being a lot shorter than the collection cycle which on large projects can be measured in months rather than days. As a consequence, they are more likely to tap the markets for an equity top up and profit growth can’t always match revenue growth because of growing interest expenses. In Cardno’s case gearing is reasonable at 55% (June 06 figure, net debt) but interest cover is good at more than 5x so they could take on a bit more debt. Once the growth phase slows and investment in working capital stabilises the firm should be able to generate more surplus cash and paydown debt fairly quickly.

I think it’s expensive at over $6.00 having run up strongly in the past couple of months but I’m interested enough to add it to the watchlist and keep working on my research. If the growth embedded in the price comes back to low-mid double digits or new information comes to light I’ll be interested.

Tuesday, February 6, 2007

Qantas bid price versus market

Investors betting that the Qantas deal will go ahead might be a bit more cautious this week following the bidders’ announcement they will voluntarily seek Government approval.

Since the bid was announced Qantas has traded at around a 5% discount to the $5.60 offer price. This discount mostly reflects the time value of money – buy the stock now at $5.37 or thereabouts and receive your money after the offer closes in March (or later if extended) – but also takes into account some uncertainty about whether the bid will actually go ahead.

For an investor thinking about arbitraging between the market price and the bid price it’s important to think about the possible downside risks compared to the fairly small upside. Consider Coles’ share price after they announced on October 19, 2006 the rejection of KKR’s buyout offer: down 9% in one day.

Looking at Qantas’ previous trading levels and operational performance a 9-10% fall seems to be a reasonable estimate of the downside should the bid fail, whereas the upside seems limited to perhaps 4% at last week’s close. While a Government inquiry into the bid shouldn’t result in failure it might extend the amount of time taken for the bid to go through and that makes the upside look even worse. It’s a classic ‘time value of money’ problem: would you rather have your $5.60 a share in 2 months or 4 months?

These factors explain why the market price hasn’t yet traded up to the bid level. As we get closer to conclusion they should converge.

Since the bid was announced Qantas has traded at around a 5% discount to the $5.60 offer price. This discount mostly reflects the time value of money – buy the stock now at $5.37 or thereabouts and receive your money after the offer closes in March (or later if extended) – but also takes into account some uncertainty about whether the bid will actually go ahead.

For an investor thinking about arbitraging between the market price and the bid price it’s important to think about the possible downside risks compared to the fairly small upside. Consider Coles’ share price after they announced on October 19, 2006 the rejection of KKR’s buyout offer: down 9% in one day.

Looking at Qantas’ previous trading levels and operational performance a 9-10% fall seems to be a reasonable estimate of the downside should the bid fail, whereas the upside seems limited to perhaps 4% at last week’s close. While a Government inquiry into the bid shouldn’t result in failure it might extend the amount of time taken for the bid to go through and that makes the upside look even worse. It’s a classic ‘time value of money’ problem: would you rather have your $5.60 a share in 2 months or 4 months?

These factors explain why the market price hasn’t yet traded up to the bid level. As we get closer to conclusion they should converge.

Sunday, February 4, 2007

Portfolio management in spreadsheets

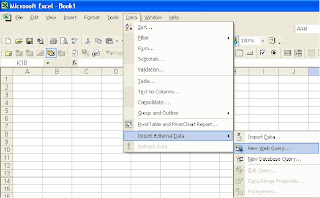

Following the post on portfolio construction I received a question from someone about how to setup a worksheet to obtain ‘real time’ values for shares and managed funds.

It’s quite straight forward as it’s a standard function in Excel. What you need to do is go to the Data menu in Excel and choose Import External Data, then New Web Query

In the box that appears navigate your way to whatever website you want to use e.g. ASX for share prices, or say Platinum’s managed fund prices

Let’s say we’re going to the ASX:

Enter in your stock codes in then once you get there tick whichever of the yellow boxes contains the information you want

Once you import the data you can set options around when it refreshes and so on so it’s reasonably flexible. The downside is that a lot of the data pulled down by some of the queries is more than you need – I put my ASX data onto a separate sheet and then use VLOOKUP formulas on my portfolio sheet to find what I want.

It’s obviously easier than entering numbers in manually and having to navigate to several different fund manager websites. Although my margin lender provides online portfolio access the managed fund prices are usually well out of date and I also have shares that aren’t in the margin loan portfolio.

Thanks again for your feedback, keep it coming!

It’s quite straight forward as it’s a standard function in Excel. What you need to do is go to the Data menu in Excel and choose Import External Data, then New Web Query

In the box that appears navigate your way to whatever website you want to use e.g. ASX for share prices, or say Platinum’s managed fund prices

Let’s say we’re going to the ASX:

Enter in your stock codes in then once you get there tick whichever of the yellow boxes contains the information you want

Once you import the data you can set options around when it refreshes and so on so it’s reasonably flexible. The downside is that a lot of the data pulled down by some of the queries is more than you need – I put my ASX data onto a separate sheet and then use VLOOKUP formulas on my portfolio sheet to find what I want.

It’s obviously easier than entering numbers in manually and having to navigate to several different fund manager websites. Although my margin lender provides online portfolio access the managed fund prices are usually well out of date and I also have shares that aren’t in the margin loan portfolio.

Thanks again for your feedback, keep it coming!

Saturday, February 3, 2007

Why I sold one of my small cap stocks this week

This week I sold out of one of my small cap stocks, a small Australian manufacturer. I bought into them in December 2005, attracted by strong dividends – a yield of 10%, fully franked – that were fairly well covered by earnings, and my assessment the shares were worth perhaps 95 cents instead of the 76 cents I paid. This assessment was made using an EBIT multiple relative to similar companies. In hindsight I think it was flawed and I should have used DCF (see an earlier post for more info.

Growth prospects were reasonably good in their sector and in adjacent markets; the company possessed some new technology that customers were in the process of adopting.

Of course, high yield generally reflects higher risk and this case was no different. Two customers – notorious hard cases for their suppliers – represented 80% of revenue. But the firm was diversifying and actively growing alternate revenue streams from ‘bolt on’ acquisitions.

I saw the yield as my reserve chute; even if the capital gains didn’t materialise in the next 12 months I could be happy to sit on it provided the yield wasn’t put at risk.

However patience finally got the better of me. In late January – 3 or 4 weeks from the next reporting date – the dreaded asterisk next to the stock code…and the “trading update” header on the announcement. Yep, profits going to be down for various reasons, and dividend to be cut. Since that was my primary reason for holding the stock I put the sell order in straight away, but not before it had lost 10%. Luckily, it had put on some capital gain recently and the 10% brought it back, literally, to my entry level. I made a grand capital gain of $0.35, but also kept my dividends which gave me an IRR on the stock of about 13%. It’s not a wipeout by any stretch but the market’s put on over 20% in the same time frame and I did have two opportunities to get out close to 90 cents but greed got the better of me.

I’m reminded of some important pieces of investment wisdom – taking these on board earlier would have resulted in a tidy overall return, ahead of the market.

Overall a good reminder and I was lucky to still come off in front.

Growth prospects were reasonably good in their sector and in adjacent markets; the company possessed some new technology that customers were in the process of adopting.

Of course, high yield generally reflects higher risk and this case was no different. Two customers – notorious hard cases for their suppliers – represented 80% of revenue. But the firm was diversifying and actively growing alternate revenue streams from ‘bolt on’ acquisitions.

I saw the yield as my reserve chute; even if the capital gains didn’t materialise in the next 12 months I could be happy to sit on it provided the yield wasn’t put at risk.

However patience finally got the better of me. In late January – 3 or 4 weeks from the next reporting date – the dreaded asterisk next to the stock code…and the “trading update” header on the announcement. Yep, profits going to be down for various reasons, and dividend to be cut. Since that was my primary reason for holding the stock I put the sell order in straight away, but not before it had lost 10%. Luckily, it had put on some capital gain recently and the 10% brought it back, literally, to my entry level. I made a grand capital gain of $0.35, but also kept my dividends which gave me an IRR on the stock of about 13%. It’s not a wipeout by any stretch but the market’s put on over 20% in the same time frame and I did have two opportunities to get out close to 90 cents but greed got the better of me.

I’m reminded of some important pieces of investment wisdom – taking these on board earlier would have resulted in a tidy overall return, ahead of the market.

- Don’t buy businesses with bad economics – this particular case the company didn’t have any pricing power with their suppliers and were forced to increase their working capital quite a bit (i.e. using up more cash) when one of the major customers simply decided to lengthen payment terms

- If your primary reasons for holding a stock or position change, then change your position

- Cross check your valuation – whether it’s with a broker’s report or by using another method, don’t just rely on multiples or DCF

Overall a good reminder and I was lucky to still come off in front.

Thursday, February 1, 2007

Economists bring back the biff

Economists aren’t the sort of people you’d have at the top of your dinner party invite list. Sure, JM Keynes might entertain your guests with wit and wisdom while Stephen Levitt – of Freakonomics fame – could astound and confront them with his work on society but on the whole it’s not the most exciting of professions…or so I thought until I read an article in today’s paper.

Under the heading “Vengeful hacker wins reprieve” the Australian Financial Review (

For those not familiar with the tale, after leaving Access Economics, Mr Rothfield joined ACIL Tasman and subsequently hacked into Access’ email system, downloading confidential documents including copies of tenders that both companies were working on. Exciting stuff, cybercrime, industrial espionage, economics, all rolled up into one.

But for my money, the real entertainment (as an interested outsider) came from the judges comments about Mr Rothfield. According to the AFR the judge found that

While his feelings about AE were jaundiced, they were aggravated by feelings of abandonment caused by a lonely upbringing and estranged parents.

But wait, there’s more. The Fin went on with judges comments including the pearler:

…while his history of emotional neglect meant he struggled to fit into work environments, he would be [my emphasis] well suited to an academic career

And lastly, just in case you still couldn’t believe your eyes

[the judge] described his PhD, on underground electricity cabling, as important work that he should be free to continue

Hats off to the AFR for keeping a straight face and not inserting any (not one!) smart alec comments into the story!

Victorian County Court judgements are normally posted here but this particular case wasn’t up just yet.

Sunday, January 28, 2007

Building a portfolio from scratch

In late 2003 and early 2004 as the market emerged from a period of malaise I began to get more serious about putting together a reasonable investment portfolio. I really wanted to get some scale and some structure rather than the fairly rag-tag random bunch of stocks and cash holdings I held. I also was – and remain – primarily interested in shares rather than bonds or property.

This is because I really have trouble paying what I think are massive entry/exit costs for investing in direct property – not to mention the ongoing maintenance or fees payable – and bonds, frankly, aren’t that exciting. That said, no doubt bonds will have their day in the sun some time in the next couple of years as I think Aussie rates will begin to fall.

Looking back, after several years of really strong market performance, it’s interesting to review the decisions and seek improvement. For anyone who does want to get serious about putting together a decent investment portfolio I hope there might be some ideas or help here. Firstly, here's how the asset allocation looks now:

I started with a sliver of my own equity – and I do mean a sliver, only a very small amount – comprising shares and a bit of cash, to which I added a margin loan. My initial LVR was 67% versus a loan limit of around 70% so there was some risk that a short term market correction could have screwed everything up.

I considered a number of risks that would be common to many other retail investors, and considered how I could manage them. My primary concerns were:

- Not earning at least a market return (particularly with a margin loan) – this was equally a concern for buying into a managed fund as individual stocks

- Buying at a peak and having to suffer for a couple of years

- Lack of confidence in my stock selection methods

- An unwillingness to pay entry fees on managed funds – it’s a total waste of money at with some of them looking to charge up to 4% expensive

- Dealing with a margin call

I decided to deal with point 1 by putting just over 50% of the margin loan proceeds into Vanguard’s Australian share index fund with the remainder into an Australian industrial share fund, avoiding the entry fee on the latter by downloading the forms from their website. I spent a fair bit of time thinking about whether it was better to put all into the index fund or to chase some of the other ‘hot’ managed funds at the time. I decided that it was preferable to go for the index fund because of the gearing. I felt that in my situation I simply couldn’t run the risk of an underperforming fund manager in a bull market. I think this is a common fear for many investors that I’ve spoken to.

For point 2, I decided that a key part of my strategy would be to add to my investments regularly although I didn’t setup a regular savings plan with the managed funds, preferring to pick and choose where the money went each quarter. Three months gave me enough time to save a reasonable amount.

Point 3 was interesting. Of additional investments made since commencement, maybe 30% have been in managed funds – actively managed international shares – so I’ve been selecting local stocks to fill the rest. I’ll deal with how that has gone in a later entry, but suffice to say I am a lot happier with my methods now: bull markets are great for confidence.

I wasn’t that worried about margin calls but I maintained – and still do – cash readily accessible just in case. I have a worksheet linked up to the ASX and fund manager websites so I can get valuations almost real time (if necessary – it’s not) and my key risk measures are LVR and % fall to trigger a margin call. It’s easily managed.

As far as operating the portfolio I’ve tended to reinvest distributions/dividends where possible. As mentioned, maintaining a watch on LVR means I have targeted a gearing of 55-60% so when it slips under I can add to investments. If it goes over too much I just work to bring it down.

There’ve been a few hiccups on the administrative side and I have learned to follow up every written instruction to my margin lender with a phone call.

Overall I'm quite happy, the original 'sliver' of equity has increased by almost 7x on the starting point (this includes capital gain, income and savings contributed to the portfolio).

My focus now is to continue increasing my exposure to international equities, a strategy that I began in 2005/06 and have been pursuing for as long as the AUD remains strong. As mentioned above, I have the view that the differential between local and overseas rates will fall in the near term – 12 months – causing the AUD to fall as well. I’m buying internationally-orientated companies and actively-managed international share funds. Additional investment on the ASX is on a very stock specific basis right now.

Comments and questions welcome

Tuesday, January 23, 2007

BHP - what's it worth?

Looking up BHP I’ve found that of 15 brokers submitting their estimates to Thomson Financial, 6 have it as a ‘strong buy’, 7 as a ‘moderate buy’ and 2 say ‘hold’. The median EPS forecast for 2007 is 286.3 rising to 294.2 for 2008. So it looks like that BHP, trading at $25.33, is on a forward PE of just 8.8x. By comparison,

Yet BHP has underperformed the All Ords in the last 12 months – yes, in one hell of a commodities boom, the chief commodity company on the bourse hasn’t delivered a market return. And it’s not just underperformance, BHP shares basically haven’t moved since Jan-06 while the market has put on perhaps 18-20% (BHP in blue, All Ords in red in graph below from Yahoo Finance)

There could be a few reasons for this. Maybe it’s just cheap, taking a breather after performing well the prior year, or is this just indicative of a market at the top of the cycle where PE ratios are low because the market doesn’t think earnings are sustainable. I am probably leaning toward the latter.

One of my favourite tactics when assessing if a company is cheap or not is to reverse engineer the share price, that is, what sort of growth rate is factored into the current price? I was at a presentation from Investors Mutual where they talked about how they use a variant of this strategy and identified that stocks like CSL and Brambles were effectively priced for 0% sales growth over the next 10 years. I’ve also used it successfully for stocks such as Super Cheap Auto recently and, believe it or not, Telstra.

I’ve used figures from a major institutional broker as the backbone of my own ‘back of the envelope’ calculations for BHP (note that the broker’s DCF valuation for BHP is $20.92 and they have a ‘neutral’ rating). Anyway, using the broker’s figures out to 2011 as a base then applying a simple growth factor beyond, and calculating a terminal value, it tells us that to justify a price of $25.33, BHP only needs to grow free cash by 2.5% p.a. from 2007 to 2016 (assuming an AUD/USD rate of 0.7850). Increasing the annual growth of free cash flow over the period to 3.5% increases the current value to $26.85 or +6%.

These aren’t demanding growth targets but commodities are by nature a volatile market; witness the large swings in prices of copper, for example, on a regular basis. I’ll be keeping an eye on the former Big Australian to see how things pan out. Maybe the shares will outperform in 2007, keeping the tipsters in bread and soup for another year.

Subscribe to:

Posts (Atom)